In an investment world obsessed with high-risk, high-reward strategies, the humble Certificate of Deposit remains one of the most reliable tools for wealth preservation and steady growth. But even this conservative instrument requires strategic planning to maximize its potential. That’s where a CD calculator becomes indispensable—a digital ally that transforms vague financial goals into precise, achievable targets.

A CD calculator does more than crunch numbers; it provides the clarity and confidence needed to commit your money for fixed periods. When you can see exactly how much you’ll earn, when you’ll earn it, and what factors might affect your returns, the decision to invest becomes significantly easier. In 2026, with economic uncertainty still lingering, this clarity is worth its weight in gold.

Whether you’re building an emergency fund, saving for a major purchase, or creating a stable income stream in retirement, a CD calculator should be the first tool you reach for. Discover the power of precise financial planning with the professional CD calculator at Chronological Calculator.

Setting Financial Goals with Your CD Calculator

Every successful savings strategy begins with clear goals, and a CD calculator helps you translate those goals into concrete action plans. Are you saving $50,000 for a home down payment in three years? A CD calculator will tell you exactly how much you need to deposit today and what rate you need to earn to reach that target.

The reverse calculation is equally valuable. If you have $30,000 to invest and want to know what it will grow to in various scenarios, a CD calculator can run multiple projections simultaneously. You might discover that a 2-year CD at 5.00% gets you close to your goal, while a 3-year CD at 4.75% with monthly contributions gets you there faster.

A CD calculator also helps you set realistic timelines. If your goal is $100,000 and you can only invest $20,000 now, the CD calculator might show that even the best available rates won’t get you there in two years. This insight allows you to adjust your goal, increase your contributions, or explore supplemental investment options.

Goal-setting becomes precise and actionable when you use the target-amount features in the CD calculator at Chronological Calculator.

The CD Ladder: A CD Calculator’s Greatest Showcase

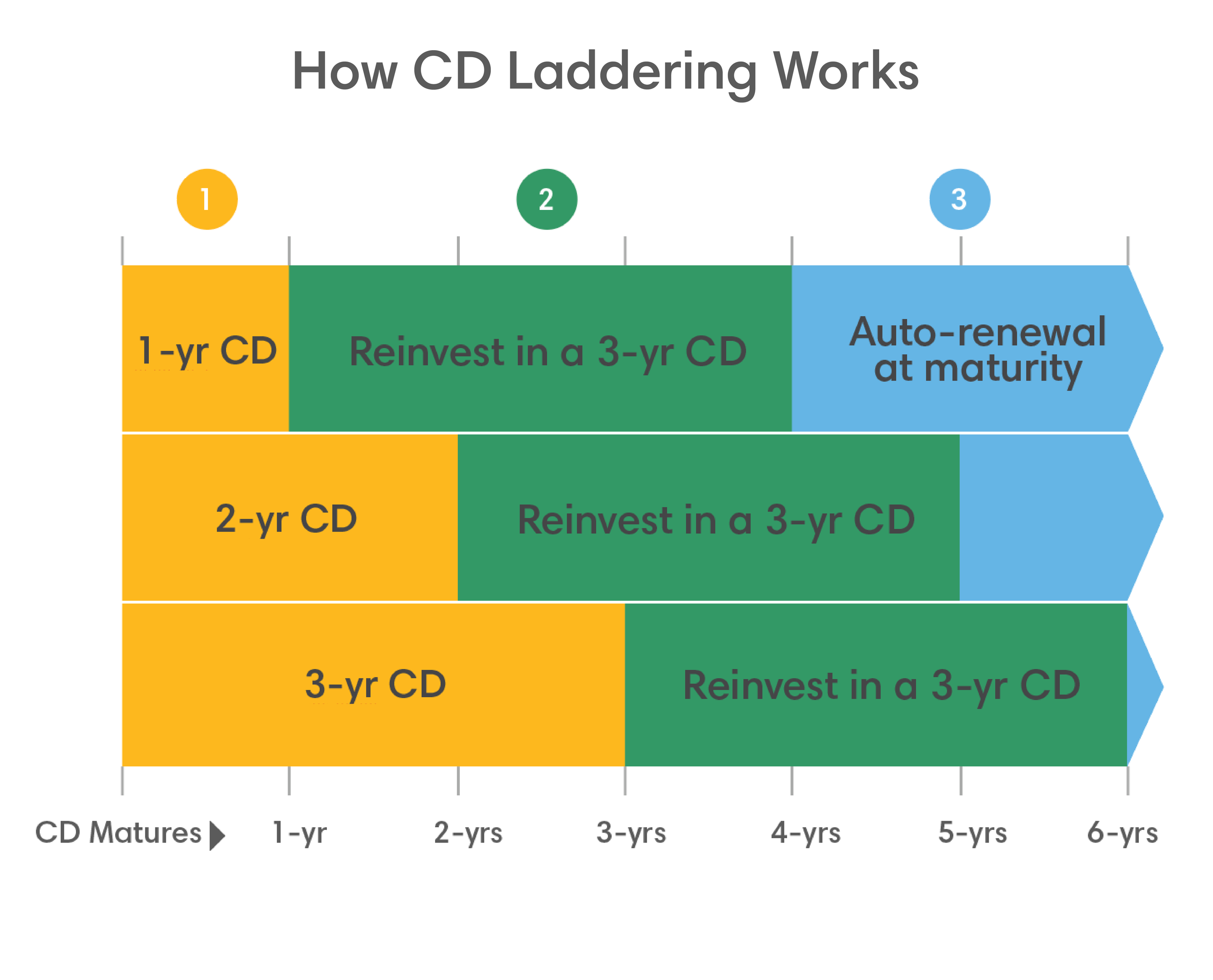

Perhaps no CD strategy benefits more from a CD calculator than the classic CD ladder. This approach involves dividing your investment across multiple CDs with staggered maturity dates, providing regular access to funds while capturing higher long-term rates.

Here’s how a CD calculator optimizes laddering: suppose you have $60,000 to invest. Instead of one 5-year CD, you might create six $10,000 CDs maturing every 6 months. A CD calculator shows you the blended yield of this ladder and how much money becomes available at each maturity date. As each CD matures, you reinvest it in a new long-term CD, maintaining the ladder’s structure.

This visual demonstrates the CD laddering concept, showing how investments mature and roll over to maintain consistent liquidity. A CD calculator takes this concept further by quantifying the exact returns at each stage. You can experiment with different ladder configurations—more rungs for greater liquidity, fewer rungs for higher average yields—and see the trade-offs instantly.

The CD calculator at Chronological Calculator includes specialized laddering tools that let you model complex multi-CD strategies and optimize your rung spacing for maximum efficiency.

Emergency Fund Optimization with a CD Calculator

Traditional financial advice suggests keeping 3-6 months of expenses in a savings account for emergencies. But with savings account rates often below 1%, many savers are exploring CD-based emergency funds. A CD calculator is crucial for this strategy because it helps you balance yield against accessibility.

Using a CD calculator, you can model a tiered emergency fund: 1 month of expenses in a high-yield savings account (instantly accessible), 2 months in a 3-month CD (slightly higher rate, short lock-up), and 3 months in a 6-month CD (better rate, manageable term). The CD calculator shows you the total yield of this tiered approach versus keeping everything in savings.

The key insight from a CD calculator is that even modest rate improvements compound significantly over time. If your emergency fund is $30,000, moving from a 0.50% savings account to a 4.50% CD ladder earns you an extra $1,200 per year. A CD calculator makes this benefit concrete and helps you overcome the psychological barrier of locking away “emergency” money.

Optimize your emergency fund strategy with the tiered modeling features in the CD calculator at Chronological Calculator.

College Savings and Your CD Calculator

For parents saving for their children’s education, a CD calculator offers a conservative alternative to volatile 529 plan investments. While 529 plans invested in stocks might offer higher long-term returns, they also carry significant downside risk. CDs provide guaranteed returns that a CD calculator can project with absolute certainty.

If your child is 10 years from college, a CD calculator can show you how a series of 1-year CDs rolled over annually will grow compared to a single 10-year CD. The CD calculator might reveal that the flexibility of annual rollovers outweighs the slightly higher rate of a long-term CD, especially if you anticipate needing the money early for private school tuition.

For students already in college, a CD calculator helps optimize remaining savings. If you have $20,000 left for senior year expenses 12 months away, a CD calculator confirms that a 1-year CD at 5.00% will generate $1,000 in risk-free interest—money that can cover textbooks, supplies, or reduce student loan borrowing.

Plan your education savings with confidence using the goal-oriented CD calculator at Chronological Calculator.

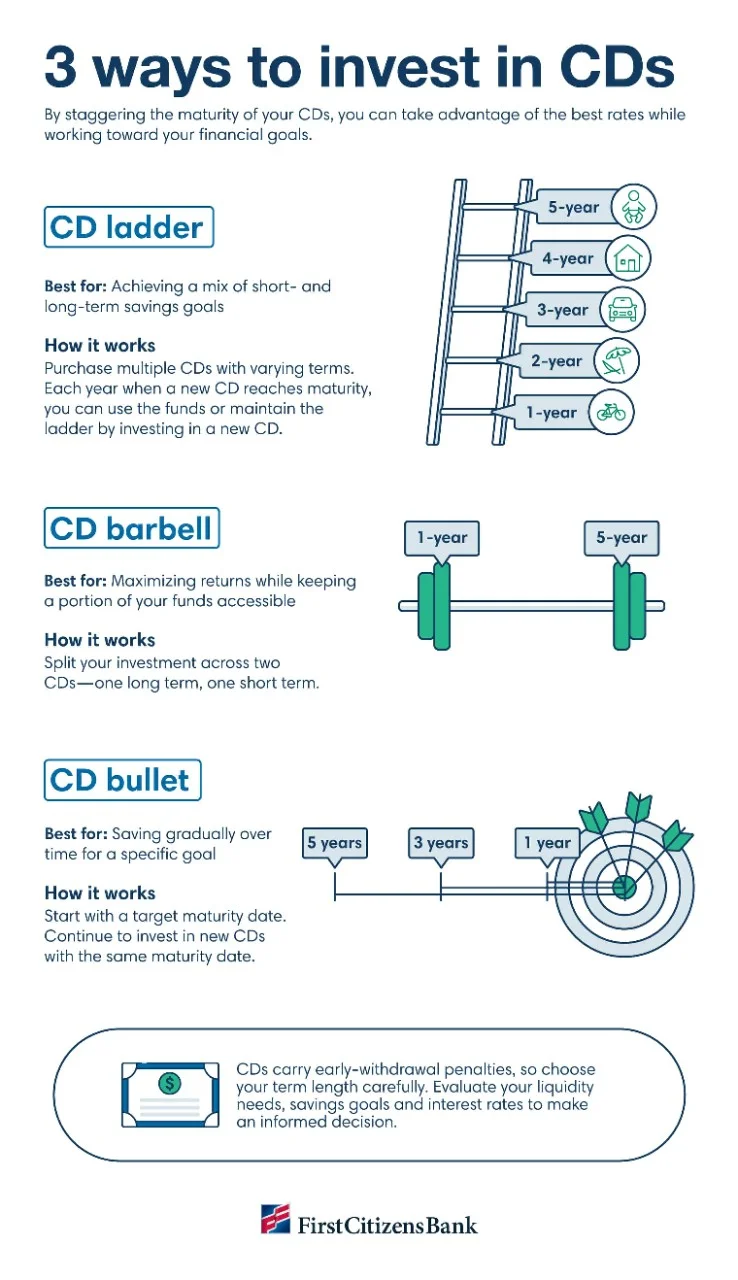

CD Barbell and Bullet Strategies: Advanced CD Calculator Applications

Beyond basic laddering, sophisticated investors use barbell and bullet strategies that a CD calculator can model and optimize.

A CD barbell strategy splits your investment between very short-term CDs (for liquidity) and very long-term CDs (for yield), avoiding medium-term CDs entirely. A CD calculator shows you the weighted average yield of this approach and how it compares to a traditional ladder. In certain rate environments, the barbell outperforms by capturing the highest short-term promotional rates while locking in long-term security.

This infographic illustrates three advanced CD strategies: laddering, barbell, and bullet approaches. A CD calculator helps you determine which strategy best fits your goals. A CD bullet strategy, conversely, involves purchasing CDs that all mature on the same future date—ideal if you know exactly when you’ll need a lump sum. A CD calculator can show you how to build a bullet portfolio by buying CDs of different initial terms but identical maturity dates.

These advanced strategies require precise calculations that only a professional CD calculator can provide. The sophisticated strategy modeling tools at Chronological Calculator make these complex approaches accessible to everyday investors.

Monitoring and Rebalancing: Keeping Your CD Calculator Updated

A savings strategy isn’t a “set it and forget it” proposition. As CDs mature and market rates change, you need to reassess your portfolio regularly. A CD calculator is invaluable for this ongoing maintenance.

Every time a CD matures, use a CD calculator to compare current rates against your existing portfolio. If rates have risen significantly, you might adjust your ladder by adding longer rungs. If rates have fallen, a CD calculator might show that extending terms no longer provides adequate compensation for reduced liquidity.

A CD calculator also helps you identify opportunities to break existing CDs and reinvest at higher rates. While early withdrawal penalties make this usually inadvisable, a CD calculator can run the break-even analysis. If you have 18 months left on a 3.00% CD and current 2-year CDs offer 5.00%, the CD calculator might show that paying the penalty and reinvesting actually increases your total return.

Stay on top of your CD portfolio with the monitoring tools in the CD calculator at Chronological Calculator.

Conclusion: Your CD Calculator Is Your Financial Compass

Building a bulletproof savings strategy requires precision, foresight, and the right tools. A CD calculator provides all three, transforming the complex world of Certificate of Deposit investing into a clear, navigable landscape. From basic goal-setting to advanced laddering strategies, from emergency fund optimization to college savings planning, a comprehensive CD calculator is the foundation of smart, conservative wealth building.

Don’t navigate your financial future blindly. Equip yourself with a professional-grade CD calculator that offers the features, accuracy, and flexibility you need to make confident decisions. Your savings deserve nothing less than the best planning tools available.

Start building your bulletproof savings strategy today with the advanced CD calculator at Chronological Calculator.