Compound interest stands as one of the most powerful forces in finance, and a CD interest calculator is the essential key to harnessing that power for your certificate of deposit investments. Whether you are saving for retirement, a major purchase, or simply building long-term wealth, understanding how compound interest works through a CD interest calculator can dramatically accelerate your financial progress. This comprehensive guide will teach you everything necessary about using a CD interest calculator to unlock the full earning potential of your CDs in 2026.

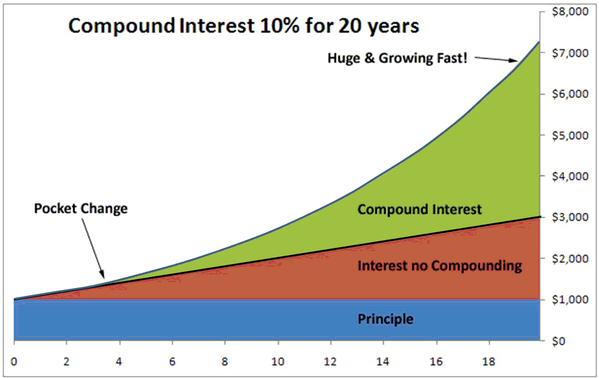

Unlike simple interest, which only pays on your original principal, compound interest allows you to earn interest on your previously earned interest. A CD interest calculator demonstrates this snowball effect in concrete numbers, showing exactly how much extra you earn through compounding. Over time, this difference becomes substantial, especially for longer-term CDs. That is why every serious saver should have a CD interest calculator bookmarked and ready for immediate use.

Understanding Compound Interest with a CD Interest Calculator

At its core, compound interest means the interest you earn gets added to your principal, and future interest calculations use this new, larger balance. A CD interest calculator applies this principle automatically, eliminating complex manual calculations. The compounding frequency—daily, monthly, quarterly, or annually—determines how quickly your balance grows, and a quality CD interest calculator lets you adjust this variable to observe its impact.

Consider a practical example. Suppose you deposit $5,000 in a 3-year CD with 4.50% APY. With simple interest, you would earn $225 annually for three years, totaling $675. However, with monthly compounding, a CD interest calculator shows you would actually earn approximately $716.15. That is an extra $41.15 simply because interest compounds. A CD interest calculator makes this advantage visible and quantifiable.

Compound Interest Formula for CDs:

plain

A = P × (1 + r/n)^(nt)

Where:

A = Final Amount

P = Principal ($5,000)

r = Annual Rate (0.045)

n = Compounding Periods (12 for monthly)

t = Time in Years (3)How Compounding Frequency Affects Your Returns

A CD interest calculator reveals that compounding frequency meaningfully impacts total earnings, though the daily versus monthly difference is smaller than many assume. Compare a $10,000 deposit in a 2-year CD at 4.50% APY:

Table

| Compounding Frequency | Interest Earned | Final Balance | Difference vs Annual |

|---|---|---|---|

| Annual | $922.50 | $10,922.50 | Baseline |

| Quarterly | $933.92 | $10,933.92 | +$11.42 |

| Monthly | $938.43 | $10,938.43 | +$15.93 |

| Daily | $940.49 | $10,940.49 | +$17.99 |

As this CD interest calculator comparison demonstrates, daily compounding yields about $18 more than annual compounding on a $10,000 deposit over two years. While modest initially, these differences compound over time. On larger deposits or longer terms, the gap widens significantly. A CD interest calculator helps you appreciate why banks compounding daily are preferable when other factors are equal.

CD Interest Calculator: Modeling Different Deposit Scenarios

One of the greatest strengths of a CD interest calculator is instant modeling of various deposit scenarios. You can answer questions like: How much must I deposit to reach $20,000 in five years? Or what APY do I need to double my money in ten years? A CD interest calculator handles these reverse calculations effortlessly.

For example, if your goal is $15,000 in three years for a new car, and you find a 3-year CD offering 4.60% APY with monthly compounding, a CD interest calculator reveals you need approximately $13,104 today. This precise goal-setting is impossible without a CD interest calculator, ensuring you save the correct amount from the start.

The Rule of 72 and Your CD Interest Calculator

The Rule of 72 provides quick mental math to estimate doubling time: divide 72 by your interest rate. A CD interest calculator verifies this rule and shows exact doubling time. At 4.50% APY, the Rule of 72 suggests doubling in about 16 years. A precise CD interest calculator confirms this is very close to actual.

However, the Rule of 72 is an approximation. For accurate planning with larger sums or specific timelines, always use a CD interest calculator. The calculator accounts for exact compounding frequency and provides precise days, months, or years to reach targets.

📌 Quick Reference: At 4% APY, money doubles in ~18 years. At 5% APY, ~14.4 years. At 6% APY, ~12 years. A CD interest calculator gives exact figures for any rate.

Tax Implications: Using a CD Interest Calculator with Tax Adjustments

Interest earned on CDs is taxable as ordinary income, meaning your actual return is lower than gross figures from a basic CD interest calculator. To see true earnings, factor in your marginal tax rate. Fortunately, many advanced CD interest calculator tools include tax adjustment features.

For example, in the 22% federal tax bracket earning $1,000 in CD interest, you owe approximately $220 in taxes, leaving $780 net. A CD interest calculator with tax integration shows this net figure automatically. Some CD interest calculator platforms even accept state tax rates for comprehensive after-tax analysis.

Holding CDs in tax-advantaged accounts like traditional or Roth IRAs changes treatment. Traditional IRAs defer taxes until withdrawal; Roth IRAs offer tax-free qualified withdrawals. A CD interest calculator designed for retirement planning models these scenarios and reveals long-term tax savings.

Inflation-Adjusted Returns: The Real Value of Your CD

A critical yet often overlooked CD investing aspect is inflation. If your CD earns 4.50% APY but inflation runs at 3.00%, your real return is only about 1.50%. A sophisticated CD interest calculator can adjust for inflation, showing your final balance’s purchasing power in today’s dollars.

This is especially vital for long-term CDs. A 5-year CD at 4.75% APY looks attractive, but if inflation averages 3.50% over five years, your real gain shrinks considerably. A CD interest calculator with inflation adjustment prevents overestimating true wealth accumulation.

Building a CD Ladder with a CD Interest Calculator

A CD ladder divides money across multiple CDs with staggered maturity dates, providing liquidity while capturing higher long-term rates. A CD interest calculator is essential for designing and optimizing ladders.

Here is how to build one using a CD interest calculator: Divide your investment into equal portions—say five for a five-rung ladder. Invest one portion in a 1-year CD, one in 2-year, one in 3-year, one in 4-year, and one in 5-year. As each matures, reinvest in a new 5-year CD. A CD interest calculator shows your ladder’s blended average rate and projects total returns over time.

The beauty is always having a CD maturing soon, providing fund access without penalties. Meanwhile, most money earns higher long-term rates. A CD interest calculator helps fine-tune rungs to match liquidity needs and return objectives.

CD Interest Calculator for Retirement Planning

Many retirees and pre-retirees use CDs as safe, predictable portfolio components. A CD interest calculator is invaluable for retirement income planning. Calculate exactly how much annual interest income your CD portfolio generates, helping budget living expenses without touching principal.

For example, with $200,000 in CDs averaging 4.50% APY, a CD interest calculator shows approximately $9,000 annual interest. If you need $40,000 yearly for expenses, your CDs cover about 22.5%, and you plan the remainder from Social Security, pensions, or other investments. A detailed CD interest calculator can even model withdrawal strategies spending interest while rolling principal into new CDs.

Comparing CD Interest to Other Fixed-Income Options

A CD interest calculator is not merely for CD-to-CD comparisons; it also evaluates CDs against Treasury bonds, municipal bonds, and high-yield savings accounts. Inputting alternative yields into a CD interest calculator reveals side-by-side earnings over identical periods.

Treasury bonds may offer similar yields with different tax treatment and liquidity. Municipal bonds provide tax-free interest at often lower rates. High-yield savings accounts offer flexibility but typically lower APYs than CDs. A CD interest calculator quantifies these trade-offs for optimal vehicle selection.

💡 Tax-Efficient Tip: In a high tax bracket, compare after-tax taxable CD yield (using a CD interest calculator with tax adjustments) to tax-free municipal bond yield. Sometimes municipal bonds win on an after-tax basis despite lower stated yields.

Automating Your CD Interest Tracking

With multiple CDs, tracking interest earnings becomes complex. Some CD interest calculator tools offer portfolio tracking where you input all CDs and see total projected interest, average APY, and maturity schedules in one dashboard. This is incredibly useful for managing ladders or large portfolios.

Advanced CD interest calculator platforms can also send maturity alerts, giving time to research reinvestment options. This proactive management prevents auto-renewal at unfavorable rates due to forgotten maturity dates.

Conclusion: Let Compound Interest Work for You

A CD interest calculator is your gateway to understanding and maximizing compound interest power. By accurately modeling scenarios, factoring taxes and inflation, and comparing options side by side, a CD interest calculator transforms CD investing from guesswork into precise science. In 2026’s favorable rate environment, there has never been a better time to put your money to work in certificates of deposit.

Do not leave your financial future to chance. Use a CD interest calculator to plan every deposit, compare every option, and optimize every decision. The compound interest earned today compounds into significant wealth tomorrow.