In today’s volatile financial landscape, finding safe and reliable ways to grow your money has become more important than ever. A CD calculator is one of the most powerful yet underutilized tools available to everyday investors who want to maximize their returns without taking unnecessary risks. Whether you’re planning for retirement, saving for a down payment on a home, or simply looking to park your emergency fund in a high-yield account, understanding how a CD calculator works can make the difference between mediocre and exceptional returns.

A CD calculator helps you determine exactly how much interest you’ll earn on a Certificate of Deposit before you commit your hard-earned money. Instead of guessing or relying on vague bank advertisements, you can input your principal amount, interest rate, and term length to get precise projections. This level of financial clarity is essential in 2026, when interest rates continue to fluctuate and competition among banks for depositors’ money remains fierce.

If you’re ready to take control of your savings strategy, start by using a reliable CD calculator at Chronological Calculator to explore your options and make informed decisions about your financial future.

What Is a CD Calculator and How Does It Work?

A CD calculator is a specialized financial tool designed to compute the future value of a Certificate of Deposit investment. Unlike standard savings accounts, CDs offer fixed interest rates for predetermined periods, making them ideal for conservative investors who prioritize capital preservation over high-risk, high-reward strategies.

When you use a CD calculator, you typically input three key variables: your initial deposit (principal), the annual percentage yield (APY), and the term length (usually ranging from 3 months to 5 years). The CD calculator then applies the compound interest formula to show you exactly how much money you’ll have at maturity. Some advanced CD calculator tools also factor in early withdrawal penalties, tax implications, and inflation adjustments to give you a more realistic picture of your net returns.

The beauty of a CD calculator lies in its simplicity. You don’t need to be a financial wizard to understand the output. Most CD calculator interfaces present results in clear, easy-to-read formats, often including visual charts that show your money growing year over year. This transparency empowers you to compare different CD offers side by side and choose the one that best aligns with your financial goals.

For the most accurate projections, we recommend using the professional-grade CD calculator available at Chronological Calculator, which includes advanced features like APY comparison and penalty estimation.

The Power of Compound Interest: Why Your CD Calculator Results Matter

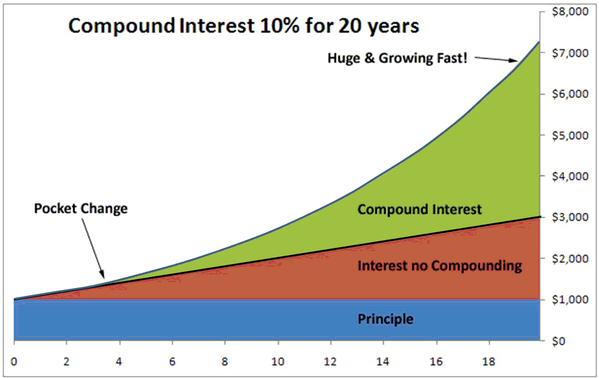

One of the most compelling reasons to use a CD calculator is to visualize the power of compound interest. Albert Einstein reportedly called compound interest the “eighth wonder of the world,” and for good reason. When you reinvest your earned interest rather than withdrawing it, your money grows exponentially over time.

A high-quality CD calculator will show you the dramatic difference between simple interest and compound interest. For example, if you invest $10,000 in a 5-year CD with a 4.5% APY compounded monthly, a CD calculator will reveal that you’ll earn approximately $2,460 in interest—significantly more than the $2,250 you’d earn with simple interest. That extra $210 might not seem like much, but over multiple CDs and decades of investing, compound interest can add thousands of dollars to your portfolio.

The chart above illustrates how compound interest accelerates wealth growth over time compared to non-compounding interest. When you use a CD calculator to plan your investments, you’re essentially harnessing this mathematical phenomenon to build wealth passively. The earlier you start and the longer you let your money compound, the more dramatic the results become.

To see exactly how compound interest will work for your specific situation, plug your numbers into the CD calculator at Chronological Calculator and watch your projected wealth grow.

Types of CDs and How a CD Calculator Helps You Choose

Not all Certificates of Deposit are created equal, and a sophisticated CD calculator can help you navigate the various options available in today’s market. Understanding the different types of CDs is crucial for making an informed investment decision.

Traditional CDs offer fixed rates for fixed terms and are the most straightforward option. A basic CD calculator works perfectly for these, showing you exactly what you’ll earn at maturity. Bump-up CDs allow you to request a higher rate if market rates rise during your term—while harder to model precisely, an advanced CD calculator can run scenarios showing potential upside. Liquid CDs offer penalty-free early withdrawals but typically come with lower rates, and a CD calculator can help you determine if the flexibility is worth the reduced return.

This infographic breaks down the different CD types available to investors. When you use a comprehensive CD calculator like the one at Chronological Calculator, you can input different scenarios for each CD type and compare the outcomes. This side-by-side comparison is invaluable when deciding between a slightly higher rate with less flexibility versus a lower rate with more access to your funds.

Brokered CDs and jumbo CDs (typically requiring $100,000+ deposits) offer even more complexity. A professional-grade CD calculator can help you determine whether the higher rates on jumbo CDs justify tying up larger sums of money. Similarly, if you’re considering a CD ladder strategy, a CD calculator becomes essential for optimizing your rungs and maximizing overall yield.

CD Laddering Strategy: Maximizing Returns with Your CD Calculator

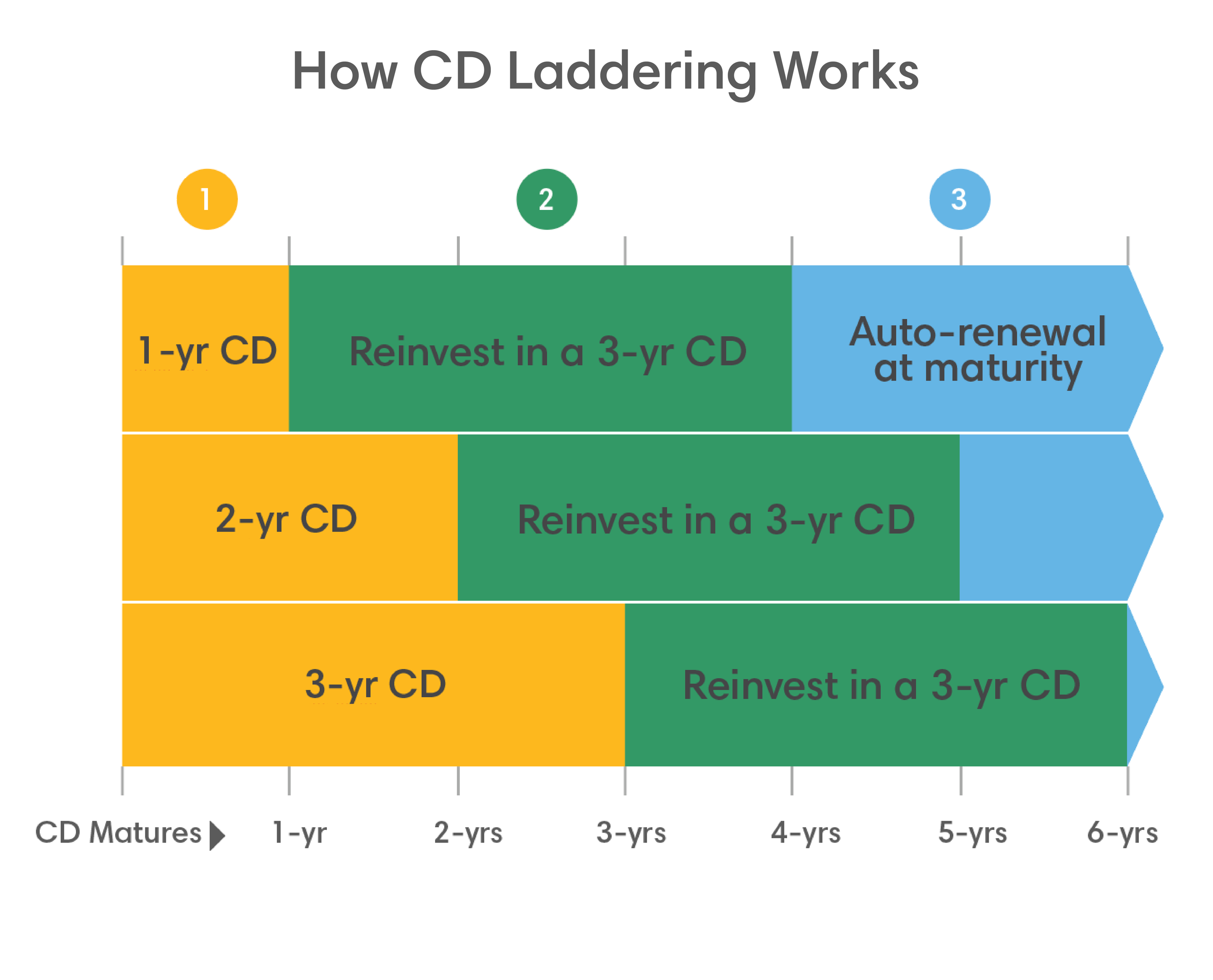

One of the most effective strategies for CD investors is called “laddering,” and a CD calculator is absolutely essential for executing this approach successfully. CD laddering involves dividing your investment into multiple CDs with staggered maturity dates, providing both regular access to funds and exposure to potentially higher long-term rates.

Here’s how it works: instead of investing $30,000 in a single 5-year CD, you might split it into six $5,000 CDs with terms of 6 months, 1 year, 18 months, 2 years, 3 years, and 5 years. As each CD matures, you reinvest it in a new 5-year CD. A CD calculator helps you model this strategy by showing you the blended average rate you’ll earn and how much liquidity you’ll maintain at any given time.

This visual guide demonstrates how CD laddering creates a continuous cycle of maturing investments. When you use a CD calculator to plan your ladder, you can experiment with different rung intervals and amounts to find the perfect balance between yield and accessibility. The CD calculator at Chronological Calculator is particularly useful for laddering scenarios because it allows you to input multiple CDs simultaneously and see your combined projected returns.

The key advantage of laddering is that you never have all your money locked away at once. If interest rates rise, you can reinvest maturing CDs at the new higher rates. If you need emergency cash, you only pay an early withdrawal penalty on a portion of your investment. A CD calculator helps you quantify these benefits and compare laddering against simply investing in a single long-term CD.

Understanding Early Withdrawal Penalties: A Critical CD Calculator Feature

One feature that separates a basic CD calculator from a truly valuable one is the ability to factor in early withdrawal penalties. Life is unpredictable, and even the best-laid financial plans can be disrupted by emergencies, opportunities, or unexpected expenses. Knowing exactly what it will cost you to access your money early is crucial for risk management.

Most banks charge a penalty equal to a certain number of months’ worth of interest if you withdraw your CD before maturity. For example, a 5-year CD might carry a penalty of 180 days (6 months) of interest. A sophisticated CD calculator will show you not just your maturity value, but also your net value if you need to withdraw at various points during the term.

When evaluating CD offers, always use a CD calculator that includes penalty calculations. You might discover that a CD with a slightly lower rate but a milder penalty is actually the better choice for your situation. This is especially true if you’re investing money that you might need before the full term expires.

The CD calculator at Chronological Calculator includes a comprehensive penalty estimator that shows you exactly how much you’d lose by withdrawing early at any point during your CD’s term. This transparency helps you make fully informed decisions and avoid costly surprises.

Tax Considerations and Your CD Calculator

Another advanced feature to look for in a CD calculator is tax-adjusted return calculations. The interest you earn on CDs is taxable as ordinary income, which means your actual return depends on your marginal tax bracket. A $1,000 interest payment might only be worth $760 after taxes if you’re in the 24% bracket.

Some premium CD calculator tools allow you to input your tax bracket and see your after-tax yield. This is particularly important when comparing CDs to tax-advantaged investments like municipal bonds or retirement accounts. A CD calculator with tax adjustments can reveal that a lower-yielding tax-free investment might actually outperform a higher-yielding CD once taxes are considered.

Additionally, if you’re holding CDs within an IRA or other tax-deferred account, a CD calculator can help you project your tax-deferred growth over decades. The compounding effect becomes even more powerful when you don’t have to pay taxes on your interest each year.

For the most comprehensive tax-adjusted projections, use the advanced CD calculator features at Chronological Calculator, which can help you understand your true after-tax returns.

Conclusion: Start Using a CD Calculator Today

A CD calculator is far more than a simple math tool—it’s your gateway to smarter, more profitable saving. In an era of economic uncertainty, having the ability to precisely project your returns, compare different CD products, and optimize your savings strategy is invaluable. Whether you’re a first-time CD investor or a seasoned saver looking to refine your approach, a CD calculator should be your first stop before making any deposit.

From understanding compound interest to planning CD ladders, from evaluating penalties to calculating after-tax returns, a comprehensive CD calculator covers all the bases. Don’t leave your financial future to guesswork. Take advantage of the powerful, user-friendly CD calculator at Chronological Calculator and start making data-driven decisions about your money today.