Most people who invest in Certificates of Deposit leave money on the table. They walk into their local bank, accept the advertised rate, and lock in their money without ever exploring whether they could earn significantly more. The difference between a casual CD investor and a savvy one often comes down to one tool: a CD calculator. This unassuming digital assistant holds the key to unlocking thousands of dollars in additional returns that most depositors never realize are available.

A CD calculator isn’t just for verifying bank math—it’s a strategic weapon that reveals opportunities, exposes hidden costs, and optimizes every aspect of your CD investing. In this comprehensive guide, we’ll explore the advanced techniques and insider strategies that transform a basic CD calculator from a simple arithmetic tool into a wealth-maximizing powerhouse.

If you’re ready to stop settling for mediocre returns and start maximizing every dollar, begin with the professional CD calculator at Chronological Calculator.

Secret #1: Rate Shopping with Your CD Calculator

The most obvious yet underutilized CD calculator strategy is systematic rate shopping. Most depositors check one or two banks and call it a day. A strategic investor uses a CD calculator to compare rates across dozens of institutions, including online banks, credit unions, and brokerage firms.

Here’s the secret: rates can vary by more than 1.00% APY between institutions for identical terms. On a $50,000 5-year CD, that’s a difference of over $2,500 in total interest. A CD calculator makes these comparisons instant and effortless. Input the same principal and term for different rates, and the CD calculator reveals exactly how much each bank’s offer is worth.

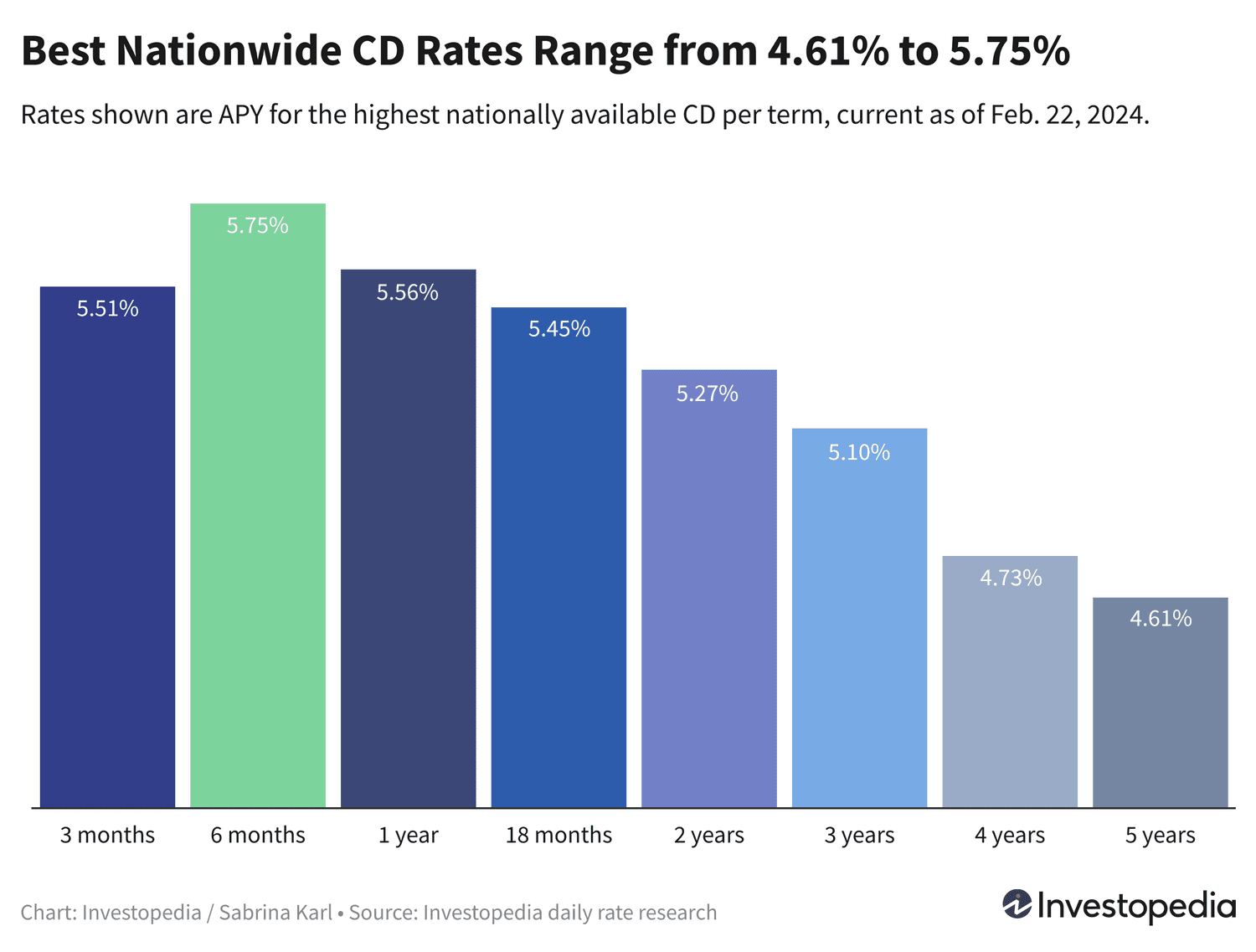

This chart shows the range of CD rates available nationwide, demonstrating why shopping around matters. A CD calculator helps you identify which institutions are offering rates at the top of this range. Don’t assume your longtime bank is giving you the best deal—use a CD calculator to verify.

Online banks consistently offer the highest rates because they have no branch overhead. A CD calculator comparison between a traditional bank’s 3.25% offer and an online bank’s 5.25% offer on a $25,000 3-year CD shows a staggering $1,500 difference in earnings. That’s real money that a CD calculator can help you capture.

Maximize your rate shopping efficiency with the comparison features in the CD calculator at Chronological Calculator.

Secret #2: The Compounding Frequency Advantage

Here’s a CD calculator secret that even experienced investors often overlook: compounding frequency can be as important as the interest rate itself. Two CDs with identical APYs but different compounding schedules will yield different returns, and a precise CD calculator captures this nuance.

Consider two 5-year CDs, both advertising 5.00% APY:

- Bank A compounds annually

- Bank B compounds daily

On a $20,000 investment, a CD calculator shows that Bank B’s daily compounding yields approximately $15 more than Bank A’s annual compounding. While $15 might seem trivial, multiply this effect across multiple CDs and decades, and the CD calculator reveals hundreds or thousands of dollars in additional earnings.

The secret is to always ask about compounding frequency and use a CD calculator that supports your bank’s specific schedule. Some banks compound continuously, others monthly, and some only at maturity. A CD calculator that assumes the wrong frequency will give you inaccurate projections.

For precise compounding calculations that match your bank’s practices, use the flexible CD calculator at Chronological Calculator.

Secret #3: Timing the Market with Your CD Calculator

While you can’t time the stock market, you can strategically time your CD investments using a CD calculator and economic indicators. CD rates closely follow the Federal Funds Rate, and by monitoring Fed policy, you can use a CD calculator to optimize your entry points.

When the Fed signals rate increases, a CD calculator can show you the cost of waiting versus locking in now. If current 1-year CDs offer 5.00% and you expect rates to rise to 5.50% in six months, a CD calculator reveals that waiting costs you approximately $250 in foregone interest on a $50,000 investment. The CD calculator helps you determine if the potential future gain justifies the certain current loss.

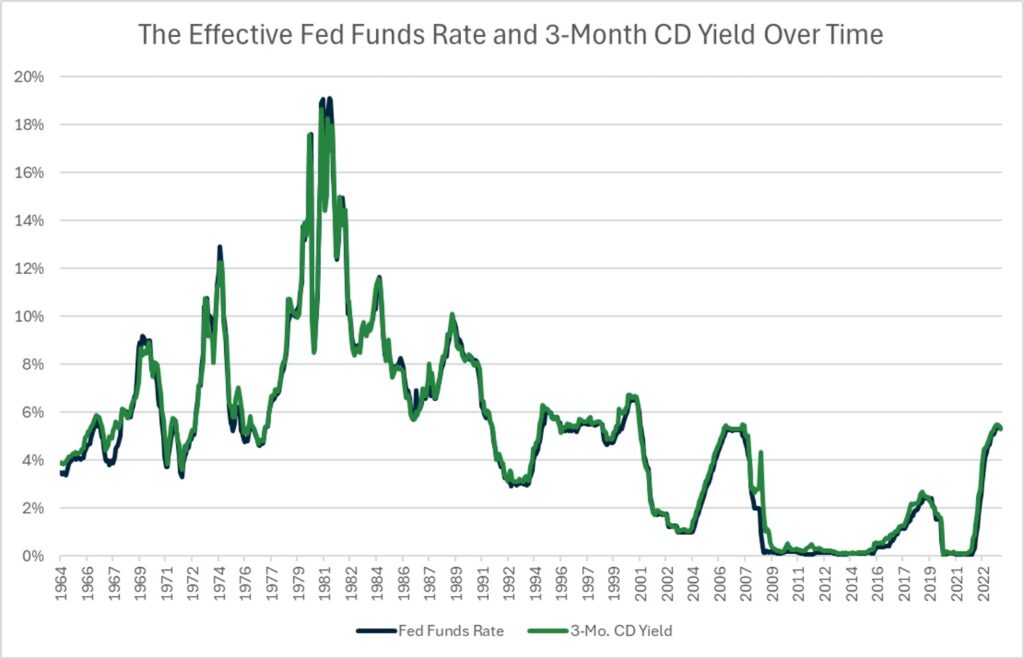

This historical chart shows the close relationship between Fed Funds Rates and CD yields over decades. A CD calculator combined with this historical context helps you make informed timing decisions. In declining rate environments, locking in long-term CDs before rates drop can preserve high yields for years. A CD calculator shows you exactly how much you save by acting quickly.

Conversely, when rates are rising, a CD calculator might recommend shorter terms so you can reinvest at higher rates later. This dynamic strategy requires regular CD calculator updates as market conditions change.

Stay ahead of rate movements with the real-time modeling capabilities of the CD calculator at Chronological Calculator.

Secret #4: Negotiating Better Rates with CD Calculator Leverage

Many depositors don’t realize that CD rates are often negotiable, especially for larger deposits. A CD calculator gives you the leverage you need to negotiate effectively by showing you exactly what competitors are offering.

Before visiting your bank, use a CD calculator to generate projections for the best available rates online. Print these CD calculator results and bring them to your meeting. When your banker sees that you have concrete data from a CD calculator showing better alternatives, they’re much more likely to match or beat those rates to keep your business.

This strategy works particularly well with jumbo CDs ($100,000+) and relationship accounts where you have multiple products with the same institution. A CD calculator showing that moving your CD to a competitor would cost them thousands in interest income is a powerful negotiating tool.

Even if your bank won’t match the best available rate, a CD calculator might show that their counteroffer is close enough to justify the convenience of staying put. The key is having the data to make an informed decision.

Generate your negotiation ammunition with the competitive rate data in the CD calculator at Chronological Calculator.

Secret #5: Tax Location Optimization Using Your CD Calculator

One of the most powerful yet underutilized CD calculator strategies is tax location optimization—placing your CDs in the most tax-efficient accounts possible. A CD calculator with tax integration reveals that where you hold your CDs can matter as much as the rate you earn.

If you’re in the 24% federal tax bracket, a CD calculator shows that a 5.00% taxable CD yields only 3.80% after taxes. But the same CD held in a Traditional IRA grows tax-deferred, and in a Roth IRA, it grows completely tax-free. A CD calculator can project the difference over 20 years, often showing that tax-advantaged placement adds 30-50% more wealth.

The secret is to use your CD calculator to compare after-tax yields across account types. You might discover that a lower-yielding CD in a Roth IRA actually outperforms a higher-yielding taxable CD. A CD calculator makes these counterintuitive insights obvious.

For investors with both taxable and tax-advantaged accounts, a CD calculator helps determine the optimal asset location. Generally, high-yield CDs belong in tax-advantaged accounts while lower-yield savings can stay taxable. A CD calculator quantifies this strategy’s impact.

Optimize your tax location with the after-tax projection features in the CD calculator at Chronological Calculator.

Secret #6: The CD Rollover Strategy That Beats the Bank

When your CD matures, most banks automatically roll it over into a new CD at the current standard rate—which is rarely the best available rate. A CD calculator secret is to always model rollover alternatives before maturity.

Three weeks before your CD matures, use a CD calculator to compare your bank’s rollover rate against the best available rates in the market. The CD calculator might show that switching banks earns you significantly more. Even if you stay with the same bank, a CD calculator gives you data to negotiate a better renewal rate.

Some investors use a CD calculator to implement a “rollover arbitrage” strategy: they intentionally let CDs mature into savings accounts, then use a CD calculator to identify promotional rates at other banks offering “new money” bonuses. These bonuses, combined with competitive rates, can dramatically boost returns.

The key is never accepting the default rollover without running the numbers through a CD calculator first. The few minutes spent comparing options can save or earn you hundreds of dollars.

Never miss a rollover opportunity by using the maturity tracking features in the CD calculator at Chronological Calculator.

Secret #7: Inflation-Protected CD Strategies

In high-inflation environments, standard CDs can lose purchasing power even while earning positive nominal returns. A sophisticated CD calculator with inflation adjustment reveals this hidden wealth erosion and helps you develop protective strategies.

One approach is “inflation laddering”—creating a CD ladder where each rung’s term length is inversely related to expected inflation. When inflation is high, a CD calculator shows that shorter terms allow you to reinvest at rising rates. When inflation stabilizes, longer terms lock in higher real returns.

Another strategy is combining CDs with Treasury Inflation-Protected Securities (TIPS) or I-Bonds. A CD calculator can model hybrid portfolios, showing you the optimal allocation between guaranteed CD returns and inflation-adjusted government securities.

The CD calculator at Chronological Calculator includes inflation adjustment features that help you protect your purchasing power in any economic environment.

Conclusion: Transform Your CD Investing with a CD Calculator

The secrets revealed in this guide share a common theme: knowledge is power, and a CD calculator is your key to unlocking that knowledge. From rate shopping and compounding optimization to tax location and inflation protection, a comprehensive CD calculator transforms passive saving into active wealth building.

The difference between an average CD investor and an exceptional one isn’t luck—it’s strategy, and strategy requires the right tools. A professional CD calculator provides the precision, flexibility, and insight needed to earn thousands more on your Certificates of Deposit without taking additional risk.

Don’t settle for the status quo. Apply these CD calculator secrets to your savings strategy and watch your returns soar. Start your journey to smarter CD investing today with the advanced CD calculator at Chronological Calculator.