When you deposit money into a Certificate of Deposit, you’re essentially lending your money to a bank for a fixed period in exchange for guaranteed interest payments. But how exactly does that interest accumulate, and how can you predict your final balance with precision? The answer lies in using a CD interest calculator—a specialized tool that demystifies the mathematics of CD returns and empowers you to make informed investment decisions.

A CD interest calculator goes far beyond simple multiplication. It accounts for compound interest schedules, varying term lengths, and different compounding frequencies to give you an accurate projection of your investment’s growth. In an era where every percentage point matters, understanding exactly how your CD interest calculator works can be the difference between a good return and a great one.

Whether you’re saving for a specific goal or building a conservative portion of your investment portfolio, a reliable CD interest calculator should be your first resource. Begin your journey to smarter saving by using the comprehensive CD interest calculator at Chronological Calculator.

How Does a CD Interest Calculator Work?

At its core, a CD interest calculator applies the compound interest formula to your specific CD parameters. The standard formula is A = P(1 + r/n)^(nt), where A is the final amount, P is the principal, r is the annual interest rate, n is the number of compounding periods per year, and t is the term in years. While you could calculate this manually, a CD interest calculator automates the process and eliminates human error.

What makes a CD interest calculator particularly valuable is its ability to handle real-world complexity. Different banks compound interest at different intervals—daily, monthly, quarterly, or annually. A $10,000 CD at 5% APY compounded daily will yield slightly more than one compounded annually, and a precise CD interest calculator captures this difference. Over a 5-year term, daily compounding might earn you an extra $50-$100 compared to annual compounding.

A professional CD interest calculator also accounts for partial periods. If you invest mid-month or your CD matures on a weekend, the CD interest calculator adjusts the interest accrual to reflect the actual number of days your money is invested. This level of precision is essential for accurate financial planning.

For the most accurate interest calculations with daily compounding and partial period adjustments, use the advanced CD interest calculator at Chronological Calculator.

Simple Interest vs. Compound Interest: What Your CD Interest Calculator Reveals

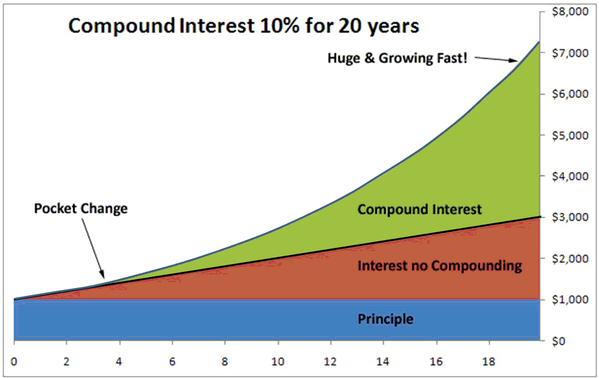

One of the most eye-opening experiences for new CD investors is discovering the dramatic difference between simple and compound interest. A CD interest calculator makes this difference immediately visible and quantifiable.

Simple interest is calculated only on your original principal. If you invest $10,000 at 5% simple interest for 5 years, you earn $500 per year, totaling $2,500. Compound interest, however, is calculated on your principal plus any accumulated interest. Using a CD interest calculator, you’ll see that $10,000 at 5% compounded monthly grows to approximately $12,834 over 5 years—$334 more than simple interest would produce.

This visualization demonstrates how compound interest creates an accelerating growth curve compared to linear simple interest. When you use a CD interest calculator to plan your investments, you’re leveraging this mathematical advantage to build wealth more efficiently. The longer your term and the more frequent the compounding, the more dramatic the compound interest effect becomes.

A sophisticated CD interest calculator will show you year-by-year growth, allowing you to see exactly when your accumulated interest starts generating significant interest of its own. This transparency helps you appreciate why longer-term CDs, despite their reduced liquidity, can be powerful wealth-building tools.

Experience the compound interest advantage firsthand by using the detailed CD interest calculator at Chronological Calculator.

APY vs. APR: Why Your CD Interest Calculator Must Distinguish Between Them

When evaluating CD offers, you’ll encounter two similar-sounding terms: APR (Annual Percentage Rate) and APY (Annual Percentage Yield). A knowledgeable investor knows that a CD interest calculator must properly distinguish between these metrics to avoid costly confusion.

APR represents the nominal interest rate before compounding. APY, on the other hand, reflects the actual annual return after accounting for compounding frequency. A CD with a 4.89% APR compounded monthly has an APY of approximately 5.00%. If your CD interest calculator only accepts APR inputs, you might underestimate your actual returns. Conversely, if you input APY as APR, you’ll overestimate.

The best CD interest calculator tools clearly label which rate type they’re using and may even convert between APR and APY automatically. This feature is particularly valuable when comparing CDs from different banks that advertise rates differently. One bank might promote their 4.95% APR, while another highlights their 5.05% APY—a CD interest calculator reveals which actually pays more.

Always verify whether your CD interest calculator is using APR or APY, and ensure you’re inputting the correct figure. The CD interest calculator at Chronological Calculator clearly displays both metrics and handles the conversion automatically, eliminating any guesswork.

The Impact of Compounding Frequency on Your CD Interest Calculator Results

Not all CD interest calculator tools are created equal, and one key differentiator is how they handle compounding frequency. The more frequently interest compounds, the faster your money grows. A CD interest calculator that assumes annual compounding will give you a different result than one that uses daily compounding—and that difference matters.

Consider a $50,000 CD at 4.5% APY over 3 years:

- With annual compounding: $57,089

- With monthly compounding: $57,178

- With daily compounding: $57,193

While the differences seem small in this example, a CD interest calculator will show that over decades and with larger principal amounts, compounding frequency can mean thousands of dollars. When shopping for CDs, always ask about the compounding schedule and use a CD interest calculator that matches it.

Some banks offer “continuous compounding,” which theoretically compounds interest infinitely often. While the practical difference between daily and continuous compounding is negligible, a comprehensive CD interest calculator should offer this option for complete accuracy.

The CD interest calculator at Chronological Calculator supports multiple compounding frequencies including daily, monthly, quarterly, and annual, ensuring your projections match your bank’s actual practices.

Inflation-Adjusted Returns: A Critical CD Interest Calculator Feature

One limitation of basic CD interest calculator tools is that they show nominal returns without accounting for inflation. A CD might promise 5% APY, but if inflation is running at 3%, your real purchasing power only grows by 2%. An advanced CD interest calculator with inflation adjustment reveals this critical distinction.

When you use an inflation-adjusted CD interest calculator, you input both the CD rate and your expected inflation rate. The calculator then shows you the “real return”—the actual increase in your purchasing power. In high-inflation environments, a CD interest calculator might reveal that your seemingly attractive CD is actually losing value in real terms.

This insight is invaluable for long-term financial planning. If your CD interest calculator shows a negative real return, you might decide to allocate more of your portfolio to inflation-protected securities like TIPS or I-Bonds, while keeping only your short-term savings in CDs.

For inflation-adjusted projections and real return analysis, use the comprehensive CD interest calculator at Chronological Calculator.

CD Interest Calculator Strategies for Retirement Planning

CDs play an important role in retirement portfolios, particularly for conservative investors who prioritize capital preservation. A CD interest calculator is essential for retirement planning because it helps you determine how much you need to save and how long your money will last.

If you’re within 5-10 years of retirement, a CD interest calculator can show you how much a “retirement CD ladder” will generate in annual income. By staggering CDs to mature each year, you create a predictable income stream that supplements Social Security and pension payments. A CD interest calculator helps you determine the optimal rung amounts to match your annual income needs.

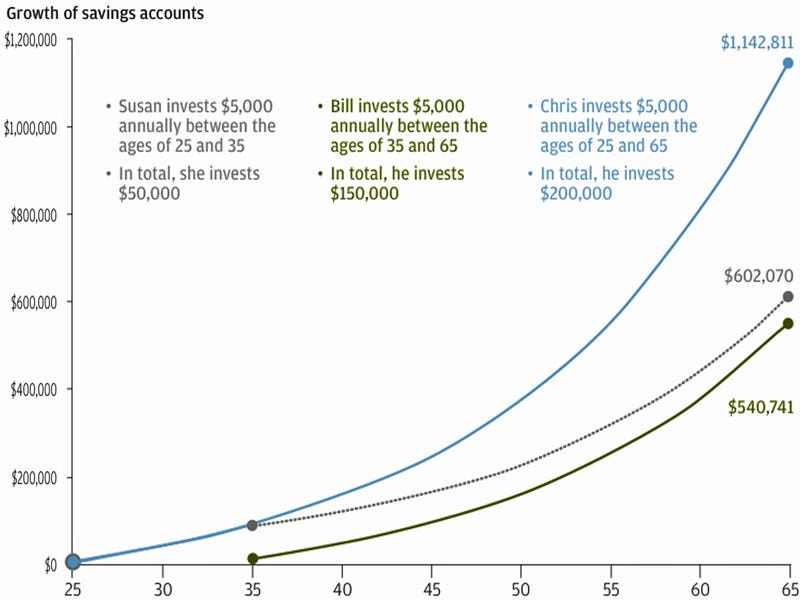

This chart illustrates how early investing dramatically impacts retirement wealth accumulation. A CD interest calculator can show you similar projections for your CD investments, demonstrating why starting early and reinvesting maturing CDs is so powerful. Even conservative CD returns, when compounded over decades, can build substantial retirement wealth.

For retirees already drawing income, a CD interest calculator helps you balance yield against liquidity needs. You might keep 1-2 years of expenses in short-term CDs and invest the remainder in longer-term CDs for higher yields. A CD interest calculator can model this barbell strategy and optimize your allocation.

Plan your retirement CD strategy with the specialized CD interest calculator tools at Chronological Calculator.

Tax Implications and Your CD Interest Calculator

The interest you earn on CDs is taxable as ordinary income, which significantly impacts your actual returns. A CD interest calculator with tax integration shows you the after-tax yield based on your marginal tax bracket. This is crucial for accurate financial planning.

For example, if you’re in the 32% federal tax bracket and your state charges 5% income tax, your combined marginal rate is 37%. A CD interest calculator will show that a 5.00% APY CD actually yields only 3.15% after taxes. This revelation might lead you to consider tax-advantaged alternatives or strategies to reduce your taxable interest.

One effective strategy is holding CDs within a Traditional IRA or Roth IRA. A CD interest calculator can compare taxable vs. tax-deferred growth, often showing that tax-deferred compounding adds 20-30% more wealth over long periods. If you have self-employment income, a SEP-IRA CD might offer even greater tax advantages.

The tax-adjusted CD interest calculator at Chronological Calculator helps you understand your true after-tax returns and explore tax-efficient CD strategies.

Conclusion: Master Your CD Investments with a CD Interest Calculator

A CD interest calculator is far more than a convenience—it’s an essential tool for anyone serious about maximizing their savings. From understanding compound interest mechanics to evaluating inflation-adjusted returns, from planning retirement income to optimizing tax efficiency, a comprehensive CD interest calculator provides the insights you need to make confident financial decisions.

Don’t settle for rough estimates or bank-provided projections that may not tell the whole story. Use a professional CD interest calculator that offers daily compounding, tax adjustments, inflation modeling, and detailed year-by-year breakdowns. Your financial future deserves this level of precision.

Start mastering your CD investments today with the advanced CD interest calculator at Chronological Calculator and watch your savings grow with confidence.